As news reports attempt to keep up with the fast-paced developments in ideas for fundamentally changing the nation’s health insurance infrastructure for low-and moderate-income Americans, we should focus on the underlying ideas driving the debates.

Paying careful attention to the language used to talk about the features of various proposals to modify the 2010 Patient Protection and Affordable Care Act (ACA) can help illuminate the consequences of proposed changes. A critical change is embedded in the seemingly minor difference in language of “universal access to coverage” and “universal coverage.”

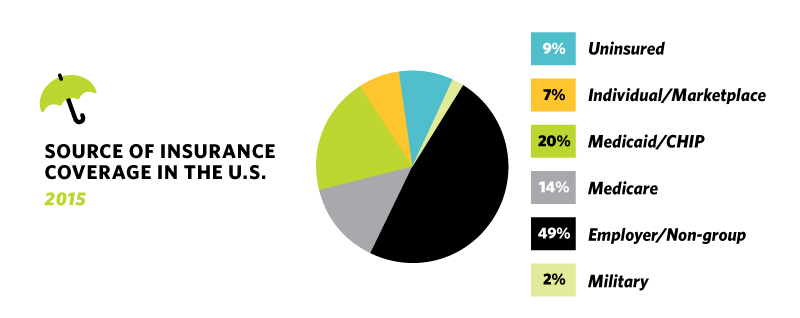

The ACA was premised on moving further down the pathway toward universal coverage. It was designed to fill the gaps in the country’s insurance system. Employment-based insurance and Medicare provide insurance for most working-age Americans and their families and the elderly. Medicaid provides coverage for low-income people. But this patchwork quilt of coverage left many gaps due to the large group of low-and moderate-income people who did not have access to employment-based insurance and whose income was above Medicaid eligibility levels (which vary by state, exacerbating the inequity).

Efforts to meet this population’s needs via an individual market for insurance have been inadequate over the past several decades. The ACA attempted to meet the insurance needs of this population in two ways: expand Medicaid to cover low-and moderate-income people at a more consistent income level across states and establish private individual insurance markets bolstered by subsidies for people with incomes above Medicaid eligibility levels. While this approach may have some practical problems, the point is the intent of the ACA is to build a system devoted to the principle that everyone should have insurance. The ACA was intended to fill in the major gaps – i.e., to move the nation toward the ideal of universal coverage.

The ideal underlying many proposals for changing the ACA is quite different, and it is often phrased as “universal access to coverage.” Universal access to coverage literally means that people will have access to buy coverage, but that insurance coverage is not an expected part of the responsibility that accompanies being an American.

Fundamentally, it is a question of our societal values and how we view health insurance – as part of a broad social compact in which we have a collective responsibility for a basic level of health and well-being for all of us, or as a product that is available to all, but is effectively rationed according to people’s ability to pay. This is the heart of the divide over the ACA, and it is an issue that deserves careful, thoughtful, reasoned debate.

It is complicated, as our current system divides us into groups when it comes to insurance coverage according to age (Medicare) or employment status (where most of us get our insurance). And the financing mechanisms used for different groups have different values and distributional effects, tilting our views about how best, if at all, we should collectively provide financing for people who cannot afford insurance coverage. Both ways of viewing health insurance can find legitimate claim to deeply held American values, and these should be made explicit and discussed. Ideally, we can find a path forward that takes the best of these values and blends them in an effective system that serves the interest of us all, but especially of those among us who have been left without health insurance for too long.